How to Buy a House with Crypto in 2026: 4 Proven Ways

Yes, you can buy a house with crypto in 2026. Four methods work today: sending Bitcoin straight to a seller, borrowing against your coins with a crypto-backed mortgage, buying a property NFT, or purchasing tokenized shares of a rental home.

The budget range is wide. A direct Bitcoin purchase requires the full property price, while tokenized fractional ownership starts from $500 on platforms like Binaryx. This guide breaks down all four ways to buy real estate with crypto: how each works, what it costs, the tax angle, and the risks nobody should skip.

Quick Summary

You can buy a house with crypto in four ways: direct Bitcoin transfer, crypto-backed mortgage, NFT deed sale, or tokenized fractional ownership from $500. Milo finances up to 100% of a home purchase against BTC or ETH collateral. Spending crypto on property is a taxable event in most jurisdictions, including the US. Deloitte projects $4 trillion of real estate will be tokenized by 2035. Below: steps, a comparison table, and a short section on buying land with crypto.

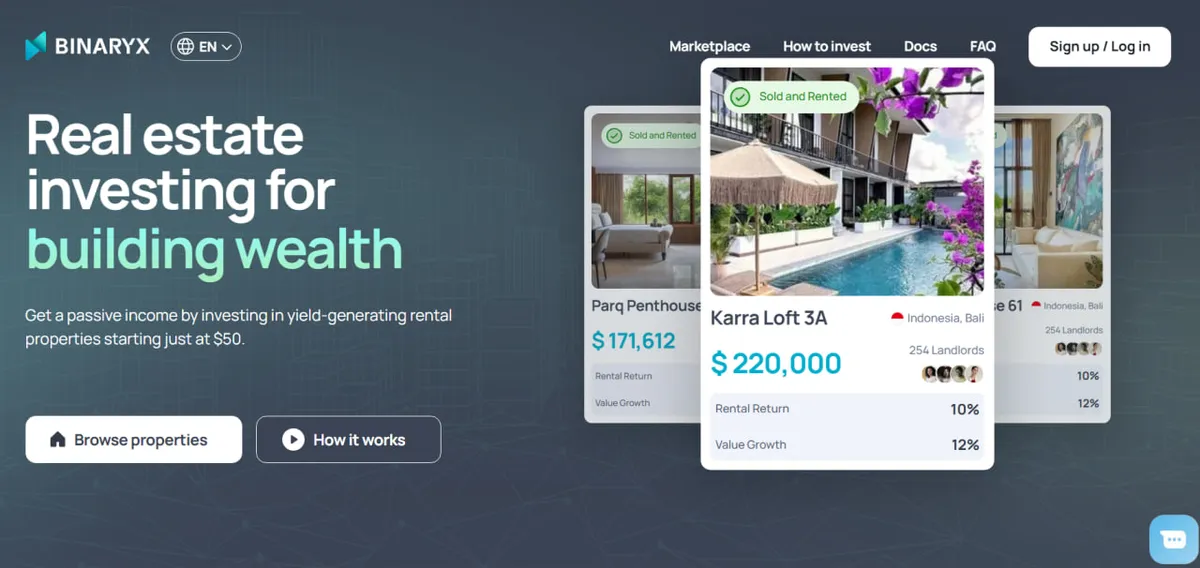

Who's behind the numbers: Binaryx (Wyoming DAO LLC, reg. 2022-001196504) is an international tokenized real estate platform operating in Bali, Montenegro, and Turkey. As of July 2026: $8,352,484 invested, 38 digitized properties, $460,003 in rent paid out, and 2,000+ investors from 70+ countries. Settlement runs in USDT or fiat on Polygon. Secondary-market exits take 20-40 minutes.

Can You Buy a House with Crypto in 2026?

Yes. Buying property with crypto is legal in most countries, and every link in the deal chain now has a crypto-ready option: lenders, escrow agents, transaction platforms, and tokenization marketplaces.

The real constraint is not technology. It is finding a counterparty and a legal structure that accept your coins. Direct seller acceptance stays rare. That gap is exactly why the three intermediated routes grew: crypto-mortgage lenders, NFT deal platforms, and tokenized ownership.

The market behind that last route is scaling fast. The Deloitte Center for Financial Services projects that $4 trillion of real estate will be tokenized by 2035, up from under $0.3 trillion in 2024 (Deloitte, 2025).

If you want the shortest path, tokenized ownership settles in minutes and needs no seller who accepts Bitcoin. You can browse live tokenized properties on Binaryx and weigh that route against the other three as you read.

Method 1: Buy a House with a Direct Bitcoin or Crypto Transfer

A direct transfer is the purest way to buy a house with Bitcoin: you send crypto from your wallet to the seller, and the seller signs over the title. Nothing in most legal systems blocks two parties from settling a property deal in BTC, ETH, or stablecoins. The purchase agreement simply records crypto as the payment method.

The process looks like this:

- Agree the price in dollars. Peg the contract to a fiat amount and fix the crypto conversion rate at closing, not at signing. Crypto prices move fast, and a dollar peg protects both sides.

- Hire a lawyer who knows both fields. Real estate law plus digital assets. The agreement must state the payment method, the wallet addresses, and what happens if the transfer fails.

- Use escrow where available. A specialized escrow agent holds the crypto until the deed records, which removes the "paid but not transferred" gap.

- Pass source-of-funds checks. Lawyers and title companies in most jurisdictions run anti-money-laundering checks on large crypto payments. Keep exchange statements and wallet history ready.

- Transfer and record the deed. The on-chain payment settles in minutes. The land registry still works at government speed.

Risks: volatility between agreement and closing, scarce sellers who accept coins, and irreversible transactions if you mistype an address. Sort out your tooling before moving six figures on-chain; our comparison of the top Metamask alternatives is a good starting point. This route suits large holders who found a crypto-friendly seller, and cross-border buyers blocked by international bank transfers.

Method 2: Take a Crypto-Backed Loan Instead of Selling

A crypto-backed loan lets you buy a house with crypto without spending a single coin. You pledge BTC or ETH as collateral, and the lender funds the purchase. Your credit history matters less than your holdings, because the collateral secures the loan.

The appeal is double. You keep your crypto position, so you still gain if prices rise. And because you never sell, you defer the capital-gains event that a sale would trigger in most jurisdictions, including the US.

Specialized crypto-mortgage lenders run this model today. Milo, one of the first such lenders, finances up to 100% of a US home purchase against Bitcoin or Ethereum collateral (milo.io, July 2026). No cash down payment, no sale of your coins.

The risk sits in the volatility. If your collateral value drops hard, the lender issues a margin call: add more crypto or face partial liquidation. A deep market crash can force the sale of your coins at the worst possible moment. Interest rates also tend to run above conventional mortgages, since the lender carries crypto risk on top of property risk.

Who is it for? Long-term holders convinced their crypto will outgrow the loan's interest, and foreign buyers without a US credit file: the collateral replaces it. If that is not you, keep reading.

Method 3: Buy NFT Real Estate (the Whole House as a Token)

In an NFT real estate deal, the house itself trades as a token. The standard structure places the property inside a limited liability company (LLC). The NFT then represents ownership of that LLC. Whoever holds the token controls the company, and the company holds the deed. Transfer the NFT and you transfer the house in one on-chain transaction.

This is not theory. In February 2022, a 2,164-square-foot house in Gulfport, Florida sold at auction for 210 ETH, about $653,000 at the time (CoinDesk). The winning bidder received an NFT tied to the LLC that owns the physical property. Propy, the platform behind that auction, still operates as a US real estate transaction service (propy.com).

The catch: everything depends on the legal wrapper. A court sees an LLC membership transfer, not a recorded deed, so you inherit any liabilities sitting inside that company. Due diligence on the LLC matters as much as the home inspection. Listings stay scarce, and lenders rarely finance NFT purchases, so buyers usually pay the full price in ETH. Treat this route as functional but niche.

Method 4: Tokenized Fractional Ownership from $500

Tokenization flips the logic of the first three methods. Instead of buying one house with a large stack of crypto, you buy fractional shares of income-generating property, starting from $500. For most crypto holders, this is the lowest-friction way to turn coins into real estate exposure.

The structure mirrors the NFT model but splits ownership into many tokens. A platform places each property in a dedicated legal entity, often a Wyoming DAO LLC, and issues tokens that represent shares. Our guide to tokenized property investing covers the legal detail. Smart contracts route rental income to token holders automatically, and you can verify your property tokens on a blockchain explorer at any time.

Here is the math on a live listing. Binaryx tokenized Hayat Green Tower in Antalya, Turkey at a $305,000 valuation, split into 6,100 tokens priced at $50 each. The platform minimum is $500 per property, and rent lands in your wallet monthly. You pay in USDT on Polygon, and the secondary market lets you exit in 20-40 minutes rather than months.

The buying process takes four steps:

- Pick a platform and pass KYC. Favor audited platforms with a secondary market. Our step-by-step guide to buying tokenized real estate compares the main options.

- Fund your account with crypto. USDT and other stablecoins settle instantly, with no bank wire needed.

- Buy tokens in the property you choose. From $500 per listing on Binaryx.

- Collect rent and exit on the secondary market whenever you decide to sell.

Trade-offs exist here too. You own shares, not a home you can live in, and your tokens live on one platform. For the economics, LLC structure, and taxes, read our fractional real estate investing guide. If the model fits your goals, open the Binaryx app to see current listings with token prices and payout terms.

Buying Real Estate with Crypto: 4 Methods Compared

Each route answers a different situation. Direct transfer maximizes control but demands a willing seller and the full price in crypto. A crypto-backed loan preserves your position and adds bank-style obligations. NFT deals compress the closing into one transaction, yet the market stays thin. Tokenized ownership drops the entry to $500 and adds rental income, in exchange for holding shares instead of keys. None of these methods forces you to cash out to fiat first, which is the point for most crypto holders. Match the method to your budget, timeline, and appetite for legal complexity. Taxes on the crypto you spend apply in most jurisdictions, so factor them into every column. Timelines below assume the paperwork side cooperates, which it rarely does on the first try.

| Method | Min budget | Timeline | Ownership form | Key risk |

|---|---|---|---|---|

| Direct crypto transfer | Full property price | Days to weeks | Title deed in your name | Volatility before closing; scarce sellers |

| Crypto-backed loan | Collateral roughly equal to the loan | Weeks | Title deed; coins locked as collateral | Margin calls and forced liquidation |

| NFT real estate | Full price in ETH | Minutes to close, weeks to prepare | LLC membership via NFT | Legal wrapper quality; thin market |

| Tokenized fractional ownership | From $500 (Binaryx) | About 20 minutes | Tokenized shares in a property-owning entity | Platform dependency; no personal use |

How to Buy Land with Crypto

Land follows the same playbook as houses, with two practical routes. The first is a direct transfer: agree a dollar-pegged price, run title and zoning checks, then settle in crypto through a lawyer or escrow agent. Land adds its own due diligence layer, since boundaries, access rights, and permitted use decide the value.

The second route is indirect. Tokenization platforms carry land-heavy projects, usually as off-plan construction where a developer builds on the plot and token holders take the project's upside. Foreign buyers should check the ownership regime first. Some markets popular with crypto buyers, Bali included, use leasehold structures for foreigners rather than freehold, so the legal wrapper does the heavy lifting.

One more difference: raw land generates no rent until someone develops it. If your goal is income rather than land banking, completed rental properties are the shorter path. The tax treatment matches houses either way: paying in crypto counts as a disposal in most jurisdictions, including the US.

FAQ: Buying Property with Crypto

Can you buy a house with Bitcoin in 2026?

Yes. You can pay a willing seller directly in BTC, pledge Bitcoin as collateral for a crypto mortgage, or convert to stablecoins and buy tokenized property shares. The limiting factor is the counterparty: few sellers accept Bitcoin, while lenders and tokenization platforms accept crypto by design.

Is buying property with crypto legal?

In most jurisdictions, yes. The deal is a standard property transaction with an unusual payment method, so normal contract and title law applies. Expect anti-money-laundering checks: lawyers, title companies, and platforms will ask where your crypto came from. A few countries restrict crypto payments outright, so confirm local rules before committing.

Do you pay taxes when you buy a house with crypto?

Usually, yes. Spending crypto counts as disposing of it, which is a taxable event in most jurisdictions, including the US, where the IRS treats it as a capital gain or loss. The gain is measured against what you originally paid for the coins. A crypto-backed loan defers this, since borrowing is not a sale. Confirm the specifics with a tax professional.

How much crypto do you need to buy real estate?

It depends on the method. A direct purchase needs the full property price in crypto. A crypto-backed mortgage needs collateral roughly matching the loan, and Milo finances up to 100% of the purchase. Tokenized ownership starts from $500 on Binaryx, with single tokens priced around $50 on specific listings such as Hayat Green Tower.

Can you buy land with crypto?

Yes: either through a direct crypto transfer with a lawyer and title checks, or indirectly through tokenized development projects built on land. Watch two things: foreign ownership rules in the country you target, and the absence of rental income until the land is developed.

Conclusion

Buying real estate with crypto stopped being exotic. Direct Bitcoin transfers close real deals where both sides agree. Crypto-backed mortgages from lenders like Milo turn holdings into housing without selling. NFT sales like the Gulfport auction prove whole homes can change hands on-chain. And tokenized platforms cut the ticket from a full house price to $500.

Pick by budget and intent. If you hold enough crypto for a full purchase and found a willing seller, a direct transfer is the cleanest path. If you refuse to sell your coins, collateralize them. If you want income and diversification instead of keys, tokenized shares deliver the fastest start. Whichever route you choose, price the deal in dollars, document everything, and treat the tax event as part of the cost.

This article is for educational purposes only and does not constitute financial, legal, or tax advice. All investments carry risk, including potential loss of principal.